Table of Contents

carterdayne

Dear Readers & investors,

Following the discussions on various outlets and forums as to how we should consider investing in this environment, I noted an overrepresentation of stances that called for protection through investing in treasuries and other so-called inflation-protected forms of investments.

I believe this can be likened to the surge of investing advice/stances that called for further growth investing in the midst of the free-money-frenzy of the past few years. While plenty of investors made money with this, most of the investors I spoke to did not harvest the profits of these investments in time, resulting in losses.

This is a different environment – but different investment environments call out all manner of self-proclaimed “experts” who claim that their strategy is a good idea for avoiding the losses many of us fear. Remember, we as humans have an extreme aversion to loss. I’ve written about human investment psychology in many of my previous broader articles.

The simple fact is that most of us aren’t emotionally built to effectively handle investing – exactly because of how emotions influence our decisions, as opposed to logic and math.

In this article, I’m going to attempt to give you the other side of the coin.

I’m going to argue against investing in treasuries.

Not investing in treasuries in an inflation environment – and why

We’re going to use some of the more popular examples here that I often see quoted as being the “best solution” – namely TIPS – Treasury inflation-protected securities.

What are TIPS?

They are government-issued bonds indexed to inflation. Thus, when we have massive inflation, as we have now, TIPS may generate superior returns not only to bonds, but even to stocks, whose linkage to inflation is either not as immediate, or not there at all. As inflation rises, TIPS are adjusted in price to maintain their actual real value.

It’s not hard to understand why these sorts of investments – or treasuries in a 3-4% interest environment – are popular. On paper, and in part in actuality, they protect you.

However, treasuries and specifically TIPS do not give what many investors believe, because most investors do not take the time to properly understand what they’re actually investing in.

So let’s do that here.

There are a number of pitfalls to TIPS or any inflation-protected security product. First of all, if the product claims to protect against inflation, the question you should begin asking is what inflation. Most of these products rely on the Consumer Price Index or CPI numbers.

This is a problem, because CPI, KPI, or whatever it’s called where you are, does not accurately state (or rarely states) actual inflation potential. TIPS or similar securities are similar to other government-sold securities. An upward adjustment of the face value also means that interest payments go up with inflation.

However, if the market expects inflation of x%, that expectation is priced into the bond market. Investors, also outside of TIPS, make decisions based on their expectations for inflation, which impacts the value of TIPS or standard treasuries – but TIPS are even less likely to outperform next to standard treasuries in this scenario.

In fact, TIPS are only likely to outperform standard treasuries if the stated CPI is higher than what the market ends up anticipating – and this theory is immediately put into question by simple fallacies/theories, such as rational expectations or the efficient market hypothesis. TIPS also have risks that traditional treasuries do not have – such as adjustments for inflation, where later adjustments for inflation can be taken back in the case of deflation (which is why recently-issued TIPS are better than older TIPS, even if the time to maturity is identical).

Deflation is a real possibility in the medium to longer term. When we had deflation (March 2020) last, TIPS ETFs and other tied securities saw significant declines.

It literally pays (or saves you) to be aware of these things.

Also, TIPS prices are relatively volatile. The characterization of these investments as “risk-free” is provably wrong. One of the major indicators of risk is price volatility, and while I’ll agree with everyone that stocks have pricing volatility, so do TIPS. Take a look at their histories in 2020 as well as back in 2008. What’s even more of a risk is that if TIPS have a substantial amount of accumulated inflation factored into their pricing levels, declines can be volatile if a deflationary depression comes.

Another misrepresentation is that TIPS returns cannot be negative. They can. If the associated interest rate rises enough to where a TIPS price declines enough for CPI inflation adjustments inherent to the security, total RoR can go into negative territory.

Schwab/Bloomberg has done plenty of research of the investment performance (in terms of RoR) under various inflation environments – going from less than 2%, between 2-4%, and higher than 4%, to see what asset classes should make for good investments in those situations.

It’s unsurprising to me that in every inflation case, the S&P500, International Stocks, and High-yield Corporates, are better performers than long-term treasuries, while S&P500 and International are better even than Treasury Bills, Muni Bonds, and mortgage-backed securities even when inflation rises above 4%. Oh, sure, the spread narrows between their outperformance. In an above-4% inflation case the RoR for the S&P500 between Treasury bills narrows to around 1.5% on an average 12-month RoR – but it’s still higher. (Source: Schwab/Bloomberg)

What can be said is that non-treasury asset classes have the potential for much higher volatility than do treasuries, TIPS and Muni bonds. The worst 12-month RoR you could see from Commodities or International stocks is a 50% drop. The worst you could see from Treasuries has never been above 8.5%, 17.1% if you include long-term treasuries.

TIPS as well as I-Bonds are popular inflation-indexed investments – but they do come with some risks and circumstances that you need to be aware of. For instance, you can only buy $10,000 worth of I-Bonds per individual – and I myself cannot buy any of these at all.

This is not me saying that you shouldn’t at all invest in Treasuries, I-Bonds, or TIPS. It’s me saying that you really need to be aware of how they work, and how they can work against you. That’s the issue I see most often.

Many people act as though they are the sort of guaranteed safeties against inflation and drawdowns, while only providing a “slight” risk. This is not at all the case, as I see it.

There is a case to be made for TIPS as protection or hedge against inflation. I just don’t see the comparative appeal to stock investing being as large as some others do.

I’ll explain why that is.

Why Stocks over treasuries

To me, it’s all a matter of how long you have. Your investment timeframe should be dictating how you allocate every cent you make.

Provided that you’re in a boat similar to mine, where you have 15-30 years until your retirement – or until you “need” the money you invest, I argue there are very few, if any reasons to invest in treasuries or TIPS. It’s the whole “not seeing the forest for the trees” sort of thing.

The current rate of inflation isn’t going to be around for all that long, I believe, given central bank responses to curbing the current rates. If this is true, then while you might eke out some momentary 5-9% gains on an annualized basis from investing in i-Bonds or TIPS, that return is going to be very short-lived once we get inflation under control.

Once this occurs, I believe that investors failing to invest in key companies and market segments currently trading at discounts will be regretting their choices.

See, to me, the next few years don’t really matter all that much.

Stocks do not offer a short-term inflation hedge, but they are excellent at hedging long-term inflation. Underlying company earnings/profits will right-size with inflation and, in the longer term, provide accurate valuation with regards to the underlying business. In the short term, the market is a voting machine – but in the longer term, it’s a value machine.

I do not care about the 1-3 year performance of investments I make today.

What I care about is making sure that:

- The company I invest in is fundamentally qualitative

- The company invests in is fundamentally safe, conservative, and well-managed.

- The company pays a well-covered dividend – the higher the better, and the longer tradition the better.

- The company I invest in can be considered cheap, both inside and outside of the current inflation environment.

- The company I invest in has a realistic upside, even in a conservative scenario, and inclusive of dividends will provide me with double-digit returns for the longer term at the valuation I invest in.

Is it perfect?

Nothing is perfect. But I consider it likely that people will continue to buy food and drink, alcohol, tobacco, water, cell phones, houses, cars, financial services, and all the other things that make our modern world spin. Because of this, invest in a well-diversified basket of high-quality providers of exactly these sort of things.

Are BASF (OTCQX:BASFY) or HeidelbergCement (OTCPK:HDELY) going to have a tough few years in this energy environment? 100%.

Is the current environment going to be the cause that these companies go into decline or even bankrupt? I’m wagering money (by investing in the companies) that this is not going to be the case.

Are their dividends covered? I believe so – even if we see small declines, this isn’t enough to obstruct my long-term thesis for them.

These are far from the only companies with this sort of thesis, or thinking. Take Comcast (CMCSA) for instance.

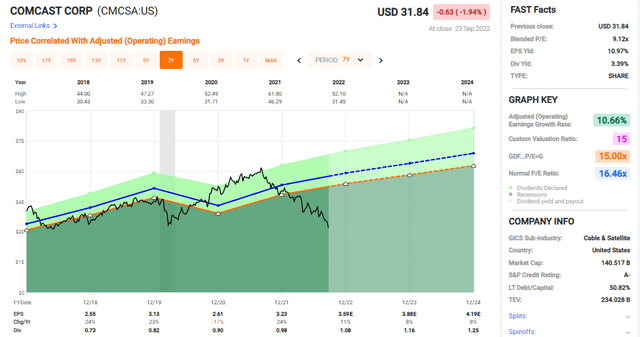

Comcast valuation (F.A.S.T. Graphs)

Issues? Some – but many? No. The company has some risks and headwinds, but recent results don’t show the pressures that the market is ascribing to the company, trading it down to a sub-10x P/E multiple despite A-rated credit and over 3.3% yield.

The upside for this giant, even ignoring its historical premium and just sticking to 15x P/E, is 40% per year until 2024E. In fact, even if you trade at exactly the same multiple in 3 years, you’d still get a double-digit RoR, in no small part thanks to the yield.

Even if initially this might not seem as safe or as good as treasuries, there are starting to be so many upsides on the market that it’s hard to keep track of them all.

I could mention dozens – even a hundred – companies that currently trade at such a discount that a long-term investment is likely to have only positive outcomes if you have a long-term timeframe.

Thinking long-term

Some of you can’t think as long-term as i. You might need the money for renovations, a new car, healthcare, pension, or other things. In that case, I can’t really give you all of my good ideas – because most of my investing is done within an extremely long timeframe.

You see, I don’t really care if the company I invest in drops 20% more, or 50%. I mean – I’d be a bit bummed about missing out on a cheaper valuation, but when I invest, I take care to only do it at what I consider attractive prices in the first place. But if BASF dropped to €1/share, I wouldn’t sell. I’d raise an eyebrow, see if I went wrong with my calculations, but provided things were still the same, I’d buy massive amounts of more.

I very rarely go for high valuations.

Plenty of my colleagues kept recommending IIPR as an investment for a long time, even when it was trading at 30x P/FFO. I wouldn’t touch the company unless it dropped below 15x P/FFO.

I’m much more likely to stake out a position in an underloved, but qualitative business with a solid yield and good management than I would be to give the “market’s darling” the time of day. I didn’t invest in tech in the recent tech bubble. I didn’t go for Bitcoin – or any crypto. I’m not investing a cent in “Hopium” companies.

In the short term, this hurts my returns, because the net effect is missing out on those market growth opportunities that seem to turn some people rich overnight.

But I am willing to pay this price in exchange for what I view as the safety of owning long-term high-quality companies. I don’t really care what the market tells me that it thinks (by giving me valuation), beyond taking advantage when the market underestimates what I invest in.

That is the core of how I currently look at things.

That’s why I remain 95%+ invested, and why most incoming capital is invested at a slow but steady rate, never allowing my cash position to rise above 5%. That’s also why my portfolio holds zero ETFs – treasury or otherwise. It’s just stocks or quality companies. My portfolio could – and has – dropped 20% or more, and i wouldn’t/didn’t bat an eyelash.

I bought more.

Part of the reason is that my living can be financed by a portion of my annual dividends alone – I’d be lying if I said that this wasn’t the case.

Value is the focus

But most of it really is my long-term timeframe.

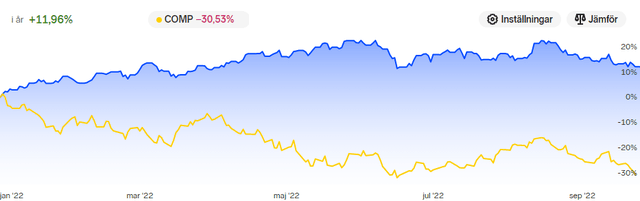

And Value investing works. While SA doesn’t like the mention of specific sums, sizes, or amounts, here is my RoR for my non-native (EU/USD/CAD) investment portfolio, seen next to the NASDAQ as a comparison.

Nordnet Author’s portfolio YTD RoR (Nordnet)

Part of it is dividends, part of it is FX, but most of that 40% spread is just picking cheap companies.

When I started investing for myself and writing about it, I promised myself that I wouldn’t chase either yield or outsized RoR in exchange for compromising on safety. I can’t claim that I’ve always managed to hold to this, as i, like anyone, have made mistakes.

But I can say that nowadays, no alluring “risky” play holds any sort of fundamental appeal for me, because I don’t “need” those outsized returns. When most investors, especially younger novices, approach the market, they immediately look for where they can generate returns of 500%, or 1000%, or even 10,000% in the shortest amount of time, often not realizing the amount of risk that goes into making such “bets”.

Me, I’ve always been happy with outperforming the market “most times”. And that’s what I’ve been doing, and continue to do, as well as target, by simply choosing attractively valued companies with great fundamentals – the better fundamentals, the more likely I am to slap money on the table.

2 Current undervalued EU stocks

It wouldn’t be a good article without some ideas – so here are two I’m currently putting money into.

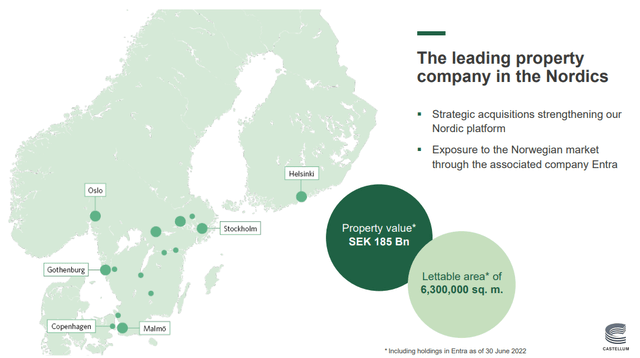

1. Castellum (OTCPK:CWQXF)

I sold Castellum (8.5%) at overvaluation when it went above 250 SEK. I promptly bought a 5% position back when it went down below 135 SEK again, and I’ve been slowly adding ever since.

Castellum IR (Castellum IR)

Castellum is a Scandinavian play on conservative, partially public-rented real estate. It’s not a REIT – Sweden does not have REITS – but it’s a RE company yielding close to 6% while renting out space to things like the Swedish Justice System, The Migration Agency, and with a mix of mixed-use and residential properties in its portfolio as well.

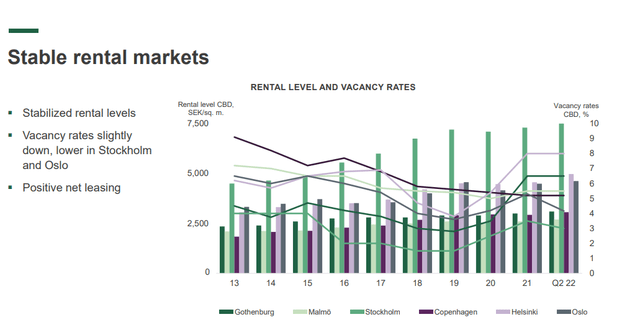

Since its IPO in 1997, the company has averaged an annual growth in property management income of 11%, and 10% dividend growth per year, corresponding to a conservative 53% P/O ratio. It’s now at a 24-year dividend tradition. The focus is on commercial properties with properties in various business categories that reflect Swedish, Danish, and Finnish business life. Customers include both private and public players, exposure to individual tenants is low and the length of the leases varies – some over 15 years, with stable rental markets as an addition. Take a look at some of these rates.

Castellum IR (Castellum IR)

The company boasts and LTV of 38.2%, and currently borrows money at an average interest rate of 1.9%, with 52% of its interest-bearing liabilities hedged at over a year. While an interest rate increase will increase costs for Castellum, this is what the company has been preparing for, for 10 years.

I consider the company a “BUY” with a native target of at least 150 SEK/share, to the current share price of around 127.

2. Airbus (OTCPK:EADSY)

As low yield as it gets, but as high-quality as it gets. Investing in Airbus is essentially investing in all of Europe, the aviation industry and space as well as the military-industrial complex across the continent.

Recent turbulence has seen a massive decline in the share price to where this A-rated Aerospace company is now trading close to 15x P/E. I’ve been loading up on a weekly basis since.

For a full thesis breakdown on Airbus and why the growth in the stock is actually very realistic, I refer you to my company-specific articles, such as this one.

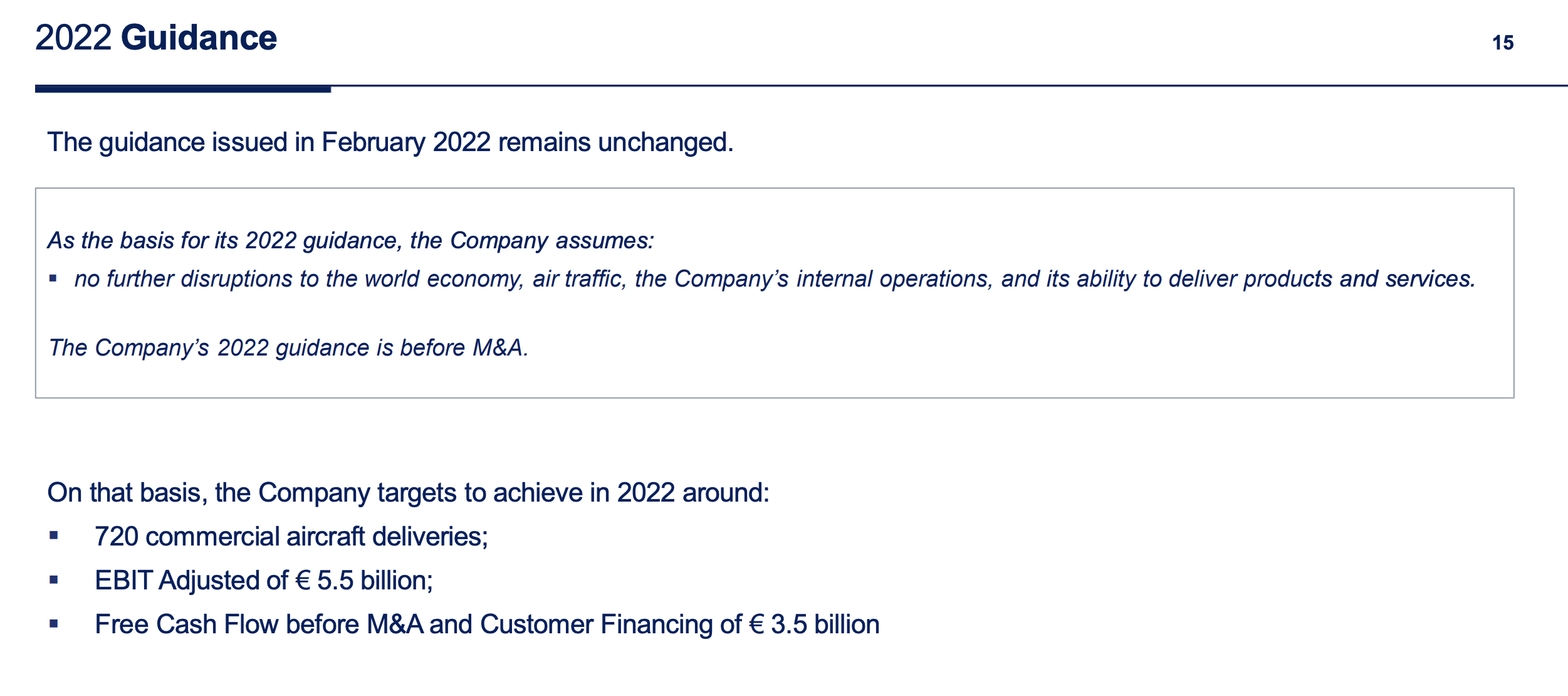

To put it simply, I believe Airbus has the potential to deliver long-term growth rates that start to touch the 200% level by 2024-2026E. Ramp-up of production and reversal as well as EPS growth that should materialize by 2023E at the latest will, to my mind, ensure that Airbus sees massive growth. Recent results have already confirmed positive EPS and EBIT, and it’s 2022E guidance remains unchanged.

Airbus IR (Airbus IR)

I fully believe that in 3 years, we’ll be looking back on Airbus and saying to ourselves “Why oh why didn’t I invest more in the company?”

That’s why I’ve established a 2.5% stake in my portfolio, and I mean to expand it to a full 5% as long as it stays cheap if my capital inflows allow for me to do so. Airbus currently has a backlog of 7,023 aircraft, including 5,821 A320 families. So with the increased production rates and the backlog intact, this gives credence to the 3-5 year overall upside for the company.

That is why I am positive about Airbus, and I believe you should take a look at the company.

Wrapping up

This is a long one, dear readers.

But it’s a subject that’s very close to my heart. Many of my friends “use” me for investment advice or ideas, and the sentiment I’ve often heard of late are questions regarding treasury investments and similar products.

I’m not fundamentally opposed to them – it’s just that they do not suit my investment goals or my investment horizon. Because this is the case, i will not touch them in any of my portfolios. Both my corporate and private portfolios are aligned with long-term goals of generating 4-5% annual yield, with the additional potential for capital appreciation.

I employ a valuation investment approach that also allows for relatively quick sales of overvalued equities. Each of my investments has trim/sell targets. I feel that my approach has garnered success not only in bull markets but in bear markets as well.

A recent example of great success is my investment in Fortum (OTCPK:FOJCF). When the company dropped below €10/share, I quickly added a large, 3% position in my portfolio with the goal of owning the company for a long time as it slowly appreciated. I could not have forecasted the fact that the company would sell Uniper (OTC:UNPPY) back to the German government, which would cause the stock price to jump above €14.1 in a matter of 28 hours.

However, I reacted and quickly sold my position for a 47.5% profit in less than 1.5 months. Many of my readers and followers on iREIT on Alpha, where I published the trades, did the same.

Why? Not because Fortum is a bad business, but because the valuation at €14.1 wasn’t at all in line with where I saw the company’s certainty and future being, especially with selling off at a loss what the company had bought for the exact reason of generating cash only a few years prior.

So I reinvested the now 47.5% larger pile of cash into better-valued and safer investments.

This is how I invest, and this is how I want to invest.

If this appeals to you, then I might be someone you want to follow.

Questions?

Let me know!