Table of Contents

")

georgeclerk/iStock Unreleased via Getty Images

While Amazon (NASDAQ:AMZN) may be an attractive option for consumers in an inflationary environment due to the price, selection and quick delivery, it has been a nightmare for the business. It looks like inflation is increasingly tough beast for Amazon to fight as it looks to continue to keep prices low and grapple with higher costs. Amazon has seen its share price decline over the year, partly due to a weaker 1Q22 as well as weaker guidance. After this deep sell-off, Amazon’s enterprise value is only $1.3 trillion. With Amazon’s 2023F AWS revenues at $130 billion, this implies that Amazon is valued at 10x AWS 2023F revenues, while assuming the e-commerce segment is worthless.

I looked deeper into the recent earnings report to find out the key positives and negatives to see if this deep valuation discount is warranted.

Investment thesis

I have written an earlier article on Amazon, which can be found here. Amazon continues to be my top large cap idea for 2022 for the following reasons:

- We will likely see meaningful margin expansion in e-commerce business due to price hikes in Prime as well as from the normalization of supply chain and fuel costs.

- Amazon’s international e-commerce business provides optionality that could bring about huge addressable markets with long runway for growth in the future.

- AWS continues to have strong industry tailwinds due to digital transformation of businesses and leverages on its industry leading position to continue to re-invest in its business and scale up.

- Advertising is increasingly gaining traction and taking market share especially in e-commerce digital marketing wallets as top global advertisers are seeing that advertising on Amazon provides value add to sellers, companies and authors.

- Amazon is increasingly becoming investor friendly as seen by growing share repurchases recently as well as stock split and improving disclosures on business segments.

- Amazon’s near term investments in fulfilment and logistics as well as in data centers continue to set the stage for long term growth as the investment spend enables the company to stay relevant in an ever changing world.

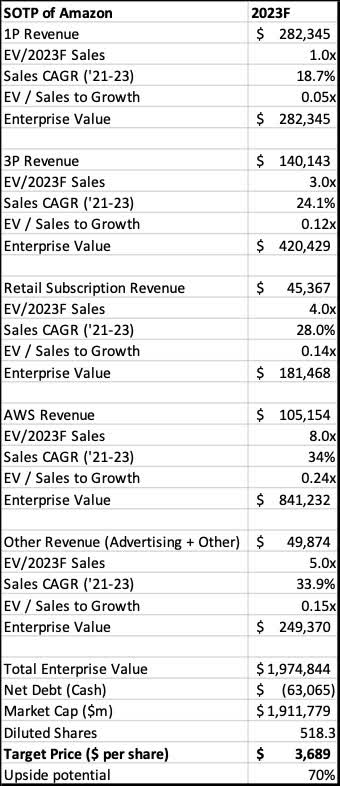

My SOTP target price for Amazon is $3689, implying 70% upside from current levels.

Key positives

AWS continues to shine and benefit from scale

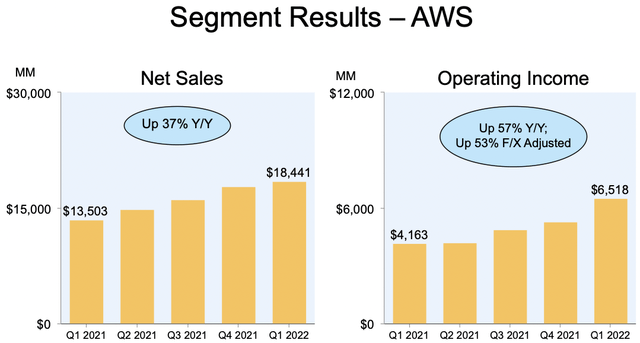

First, AWS continued to show momentum as revenue growth was 37% year on year to $18.4 billion, while operating income for the AWS segment accelerated to $6.5 billion, growing 57% year on year.

AWS net sales and operating income for 1Q22 (Amazon 1Q22)

It is clear that Amazon is the market leader in cloud as it generates more sales than the next two largest competitors combined. Even with its scale, I am of the opinion that its growth of 37% for 1Q22 is enviable when compared to that of Microsoft (MSFT) Azure or Google (GOOG) (GOOGL) Cloud’s 49% and 44% growth in the quarter.

AWS comparison with Microsoft Azure and Google Cloud (Author)

In a winner takes all market, scale is the ultimate goal and it is absolutely necessary for cloud players to win. As evident from AWS’s 1Q22 operating income growth of 57%, this demonstrates the quality growth in profitability for the cloud business when scale is achieved. With AWS operating margins at 35%, this is also largely above expectations and I am of the opinion that AWS has the potential to continue to outperform expectations on the operating margins and operating income side, while still maintaining above average revenue growth to maintain its market share in the segment.

Improving productivity and cost efficiencies

While the issues for 2021 were that of staff shortages, the shortage has no longer become an issue for Amazon. In addition, Amazon sped up capital expenditures. As such, it is good to hear from management comment that they are no longer needing to be aggressive in hiring staff as well as capacity.

While Amazon was constraint by staffing issues in 2021, and as the company continued to hire new employees during the year to make up the shortage, in 1Q22, Amazon turned from a position of understaffed to overstaffed. This lower productivity as a result of being overstaffed cost the company $2 billion in 1Q22. The company has seen improvements in productivity in the recent weeks as it looks to optimise its cost structure in accordance with the new stabilised demand.

As with physical capacity, Amazon made a conscious effort to increase capacity in the past 2 years and this resulted in a fixed cost leverage issue as it currently has excess capacity in its fulfilment network. I am of the opinion that since these capital expenditure decisions are made years in advance, management had to consider the opportunity costs of having a shortage of capacity and what that meant for the business. As such, I think that this decision to add capacity in the past 2 years was the right decision management made to ensure that capacity will not be a constraint and that its investments made today will be reaped as scale in the business continues to grow.

As such, my positive takeaway from this is that Amazon no longer has bottlenecks in labour or physical capacity. While in the short term Amazon may need to figure out how to optimise cost efficiencies with the new larger labour force and larger capacity available, I am of the view that this is Amazon investing early into improving capacity and labour to ensure that as demand continues to rise, we will see the results of these investments made in the past 2 years. We will likely see positive benefits to 2H margins as these issues progressively gets addressed and demand normalises.

Lower capital expenditures

While Amazon was chasing physical capacity and investing heavily in the past 2 years, I think we will see management not step too hard on the gas pedal as it looks to optimise the current capacity it has. As mentioned before, the heavy capital expenditure spending in the past 2 years has led to excess capacity as demand normalises post pandemic. The lower capital expenditures is positive in the near term as it looks to lower costs and optimise the existing capacity. Furthermore, I think that there is also no near term need for the capital expenditures as capacity is more than sufficient to meet demand in the near term.

Robust Prime member usage and Buy-with-Prime

Despite raising Prime rates in 1Q22, I think that its rather positive to hear from management that Amazon is continuing to see strong renewal rates for its Prime membership and that the service actually still added millions of Prime new members in the first quarter despite the price increase.

I think this also shows the strong value add to customers, and hence the reliance customers have on the Prime membership due to the wide selection of products available for Prime delivery.

Furthermore, with Buy-with-Prime, this expands Amazon’s reach to third party merchants to utilise amazon’s fulfilment network and payment options. I am of the opinion that this is a win-win situation for Amazon and third party merchants. Most importantly, for Amazon, this means higher utilisation in its fulfilment and transport networks that are currently in over capacity.

Stock buyback in the quarter

Lastly, although not often highlighted by the mainstream media, Amazon actually bought back $2.7 billion of stock in 1Q22. Recall that Amazon management has the mandate to buyback $10 billion in the company’s stock. This stock buyback provides shareholder value given that Amazon shares reacted weakly to the earnings and has been weak in the first quarter. Also, it is a decent signal to shareholders to show that the company’s management currently views Amazon stock price to be undervalued.

Key negatives

$6 billion incremental cost headwinds in 1Q22

Inflation is increasingly making it very difficult for Amazon to do business, especially for its e-commerce segment. However, there were also other factors contributing to the $6 billion incremental costs headwinds in 1Q22. Management broke this down into externally driven costs and internally driven costs.

Externally driven costs were primarily driven by inflation, adding an incremental $2 billion costs in 1Q22. This was driven by higher wage costs, higher shipping costs and fuel prices. Management said that the cost of shipping overseas is now more than 2x the pre-COVID levels, while fuel costs is also 1.5x more than just one year ago. This makes for a challenging environment for its e-commerce business as it strives to keep prices low and deliveries quick. I am of the view that this could continue to hurt Amazon for at least the next quarter, with things improving from 2H22 onwards.

Internally driven costs include productivity and fixed cost leverage, which added an incremental $4 billion in costs in 1Q22. As mentioned earlier, the lower productivity was due to overstaffing issues and the company looks to optimise the use of staff and improve this productivity sequentially from this quarter onwards. I think that this is a low hanging fruit since it is easier to control productivity issues related to overstaffing issues by reducing staff or redeploying staff to more productive uses. The fixed cost leverage issue was a result of excess capacity in its fulfilment and transport network. While this may require some cost efficiency improvements in the near term, demand also plays a factor. As e-commerce demand continues to grow and its capacity fills up, this will help to lower its fixed costs and improve the cost structure.

As management guided, this $6 billion incremental cost headwind will take time to be fully addressed, while it expected to be able to reduce this to $4 billion in the next quarter.

All in all, I expect that the controllable internal costs will likely improve quarter on quarter as management works to optimise its cost structure and improve productivity. However, uncertainties remain for the external costs as that remains largely outside of the company’s control.

Weaker guidance than expected

The guidance numbers for Amazon were top on the minds of investors as any signs of weakness could be an opportunity to sell the stock. Amazon guided for $116 billion to $121 billion revenues and operating income of -$1 billion to $3 billion, which were both worse than the fears of investors.

With this 2Q22 guidance, this implies 3% to 7% revenue growth. While this is similar to that of 1Q22, this is actually lower than the usual historical quarter on quarter seasonality. However, I think that this revenue guidance is acceptable given that the difficult comps for the company only ease in May this year. With operating income guidance, it is good to hear that the incremental costs of $4 billion were already taken into account in this guidance

Valuation

Interestingly, based on the current valuation of Amazon, it is trading at 11x AWS revenues and 36x AWS operating income, while valuing the entire e-commerce segment of Amazon at zero.

My SOTP target price for Amazon is $3689, implying 70% upside from current levels. This has taken into account weaker guidance for 2Q22, which will largely affect e-commerce top-line forecasts.

SOTP valuation of Amazon (Author created)

Risks

Competition

Although I believe Amazon has unique competitive advantage and benefits from the flywheel effect, it is not a monopoly and there is competition in both the e-commerce segment and cloud computing segment that may impact future growth in revenue and earnings and as well as potentially on the multiple Amazon should trade at. As mentioned earlier, competitors in the e-commerce space include Walmart (WMT), eBay (EBAY). In the cloud computing space, its competitors include Microsoft and Google.

Lack of scaling in its higher margin businesses

With Amazon’s advertising, cloud and third party selling and subscription business commanding the higher margins in the business, if Amazon is unable to scale successfully, this could have a material impact on its bottom line.

Unexpected investments

Although management has not yet announced any unexpected investments, should there be an unexpected investment in its many initiatives it’s focused on, this could definitely impact my margins assumptions, creating a headwind for gross and operating margins.

Volatility in the macroeconomic environment

As we have seen early in 2022, when investors risk appetite shrinks, it could impact demand for growth stocks like Amazon. Furthermore, Amazon’s e-commerce, cloud computing businesses would be impacted by shifts in macroeconomic environment should consumer or business demand wane. For example, as an enabler of online retail and with a business model that earns fees from online retail transactions, a slowdown in consumer spending could weigh on its e-commerce business.

Conclusion

While the near term challenges for Amazon remain, I think that this is an excellent chance to add Amazon shares at the current levels as it will continue to leverage on prior year investments. With its achievement of doubling fulfilment center capacity in 2 years, having a highly sticky Amazon Prime business, and without any bottlenecks in capacity or staffing, I think that this will continue to cement Amazon’s leadership in e-commerce. As it continues to leverage its scale in AWS and grow on profitability, I think that the strength from AWS will continue for many years as the growth in cloud continues. I continue to like Amazon as a top pick with increasingly positive skew on the risk reward perspective after the weakness in share price post the earnings report. My SOTP target price for Amazon is $3689, implying 70% upside from current levels.